COVID-19 and the Economy - Some Thoughts

March 17, 2020

Extraordinary.

The events we are currently witnessing are nothing short of extraordinary. The closest comparison I can make to the COVID-19 pandemic, which I have personally lived through, is September 11th. What we are experiencing now is new, it is different, and it has the potential to fundamentally change our world. Very likely there will be no going back to ‘business as usual’ when/if the pandemic passes. In the same way the world came to accept heavy screening at airports, and an endless war in the Middle East, we will come to accept new things as ‘usual’ after this pandemic.

I write this not claiming I can predict what the next months/years ahead will look like, but this is more an exercise in clarifying my own thoughts; this also serves as a time capsule, so I can look back in future years to remember what I actually was thinking during this time. Specifically, I want to focus on some of the reasons that make the stock market selloff we have seen is justified, and why, with respect to the economy, we are in scary times.

1. This is not the financial crisis

There is some good and bad in this. The good is that the solvency of banks is not really in question, and I believe the market has faith that if their solvency is called into question the central banks and national governments will not hesitate to step in to do what is necessary. We have the playbook for a financial/bank-solvency crisis, and can dust it off if it’s needed.

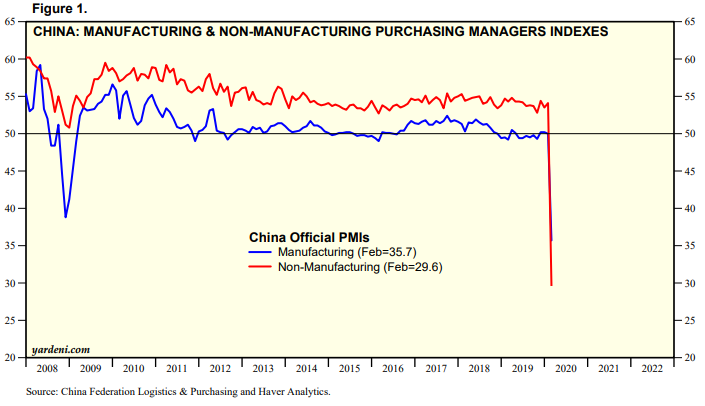

The bad is that we do not have the playbook for a sudden stop in economic activity of this magnitude. The drop in activity we saw in China is now spreading to the rest of the world. I do not believe that fiscal authorities will, or should, attempt to fully offset this decline in activity. This decline, although hopefully temporary, will be worse than what we saw in the financial crisis. In 2008-2009 the unemployment rate moved up over the course of several years. Now, in a matter of weeks several ‘non-essential’ sectors (e.g. travel, tourism, non-grocery retail) will effectively be closed. This is like having the negative employment shock of the financial crisis all at once.

2. This may not be a temporary disruption

The great assumption market is currently making is that everything returns to normal after a few months. I feel this is assumed because it is somewhat easy to model the impact of the virus this way.

The 50 day Hubei lockdown is now ending and life is beginning to return to normal. The ability for hard hit places like Hubei to return to normal will give us an indication of what the future holds for the rest of the world assuming, and this is another great assumption, the rest of the world is able to contain the virus in the same way China seems to have done. To me it seems unlikely that after such an extreme event we return to ‘business as usual’ once again. Are people really going to attend large social gatherings or eat out to the degree they did in the past? The potential permanence this shock could have on individual behaviour, and government restrictions on large social gatherings, is the first reason it is potentially incorrect to look at this as a temporary disruption.

Second, is the virus heat-resistant? There does not appear to be a definitive answer on this and the fact that there are cases of community transmission in Australia where temperatures are ~20 Celsius is not encouraging. If it is heat-resistant this could drag on into the summer.

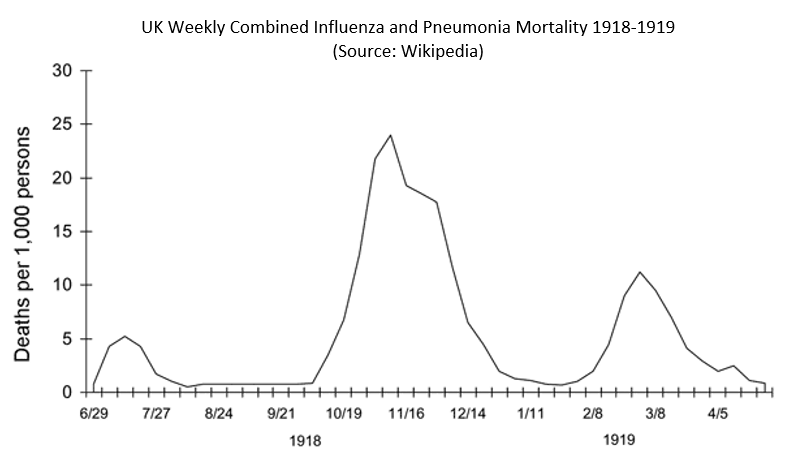

Third, what happens next winter? The Spanish influenza had multiple waves with the second being more deadly than the first. Will schools/travel/restaurants be shut down for several months next year as well? Will anyone book travel departing in the next year given this is a possibility? This seems to be a case where the answer only becomes clear with the passage of time.

Given all of these uncertainties it seems businesses will have a very hard time investing in expanding capacity, and certain industries will have a difficult time convincing lenders that will be ‘money good’ in a few months. Net-net uncertainty is likely to linger after lockdowns are ended.

3. Debt

Amid this uncertainty households and businesses have record high debt loads. This magnifies the potential impact this pandemic could have on the stock market, and economy. Government debt on the other hand is completely irrelevant since the central banks can just monetize it, and given the demand shock we are witnessing inflation is not really a problem right now.

4. A vaccine

12-18 months seems to be the timeline which a vaccine will be available. That means there could potentially be another round of lockdowns next year before something is available. I would not bet against human ingenuity in solving a crisis like this. A vaccine is the most likely way this pandemic gets sorted out.

5. Helicopter money

It will be hard for the governments to come up with ‘targeted measures’ because the sudden stop in economic activity is so pervasive. The Fed just announced ~$700bn of QE, which works out to about $2,000 for each American, and Mnuchin has floated the idea of sending cheques to Americans in the next two weeks. More interesting is to consider whether helicopter money will end when the pandemic is over. Canada first introduced income taxes during the First World War . . . as a temporary measure. After receiving free money for several months citizens may, somewhat rightly ask, why this cannot continue into the future. Is it crazy to think in an election year one of the candidates pledges to continue this when they are elected, albeit possibly in a more moderate form?

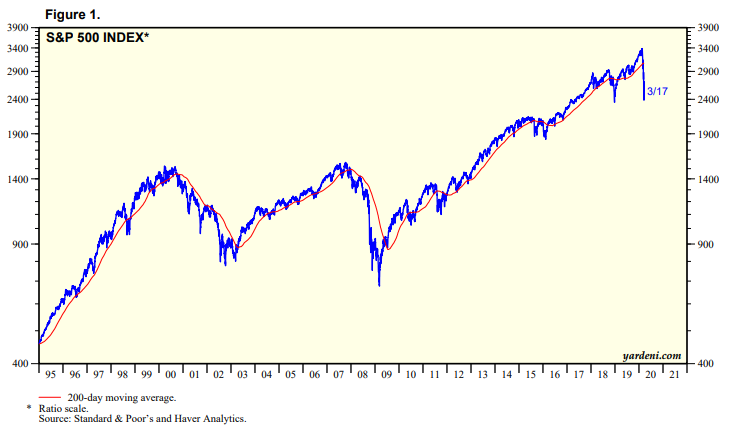

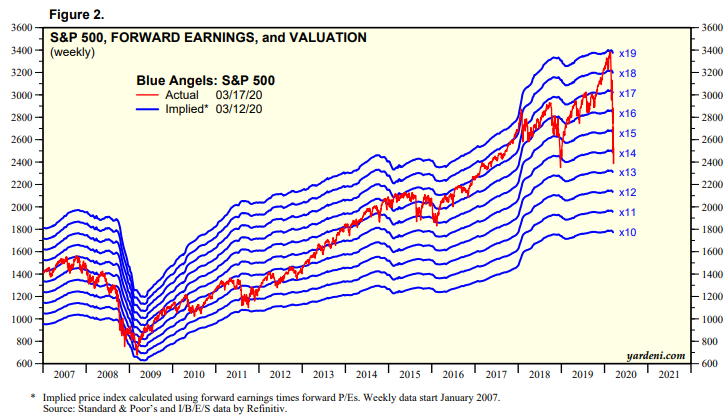

6. On Valuations

Forward PEs bottomed around 9x during the financial crisis. While it is somewhat hard to imagine that would be the case here given interest rates are so low, it would seem 10x-12x is not a crazy level to get to given the uncertainties in the market. We sit at ~14x right now (although the true number may be closer to 16x as earnings get revised).

I still think it is too early to be confident the market has bottomed, Lehman went bankrupt on 9/2008, but the market did not bottom until it was 40% lower in 3/2009.

Note: Most price/valuation charts from yardeni.com